Paying off a mortgage feels like the finish line — until you send what you think is the full amount and find out days later the loan is still open. This happens more often than most people expect, and the reason is almost always the same: the number on your monthly statement is not your actual payoff amount. If your loan is serviced by Valon, knowing exactly how the valon mortgage payoff request process works protects you from that exact situation.

This guide covers every step from start to finish. You will learn how to request your statement, what it contains, how to send your funds correctly, and what to expect once your loan is officially closed. Nothing will be left unclear by the time you reach the end.

What Is a Valon Mortgage Payoff Request?

A payoff request is a formal ask to your loan servicer for the exact dollar amount needed to fully close your mortgage. When you submit this request to Valon, they prepare an official payoff statement that reflects your true balance as of a specific date. This number is almost always higher than what your monthly billing statement shows.

The difference exists because your monthly statement only shows the unpaid principal. Your actual payoff amount also includes interest that has accrued since your last payment, any outstanding fees, and a prepayment penalty if your loan terms include one. Mortgage interest accrues every single day, so even waiting a week after your statement date changes the number.

This is not a technicality — it is a real financial difference that can leave your loan open if you send the wrong amount. Always get an official payoff statement before sending your final payment. If you want to review your current loan balance before starting, logging into your Valon account is the best first step.

When Should You Request a Valon Mortgage Payoff Statement?

Knowing when to request your payoff statement is just as important as knowing how. Many borrowers only think about this during a home sale, but there are several situations where getting this document is either required or strongly recommended.

If you are selling your home, your title company needs the exact payoff figure to settle your mortgage at closing. This is a required step — closing cannot proceed without it. If you are refinancing, your new lender’s title company will typically request the statement on your behalf, though you may need to sign an authorization form to allow access to your loan information.

Borrowers who want to pay off their loan early or consolidate debt also need an official payoff statement to send the correct amount. Even if you are just exploring whether early payoff makes financial sense, requesting a statement is completely fine. It does not commit you to anything — it simply gives you the number to work with.

One situation where a payoff request is not needed is a loan assumption. If a qualified buyer is taking over your existing mortgage rather than getting a new one, your loan does not get paid off — it transfers. In that case, no payoff statement is required because the loan continues under the new borrower’s name.

How to Request a Payoff Statement From Valon Mortgage

Getting your payoff statement from Valon is straightforward whether you handle it yourself or have a third party do it for you. You can submit the request online through your Valon account in just a few clicks, or authorize someone like a title company to request it on your behalf. Either way, Valon sends your official statement within 5 business days of receiving a valid request.

Request Through Your Online Valon Account

The simplest and fastest way to get your payoff statement is directly through your Valon online account. The process takes just a few minutes and does not require a phone call or email. Here are the steps:

- Log in to your account at valon.com

- Navigate to the Payment page

- Find the Payment Actions card

- Select Request a Payoff Statement

Valon processes your request and prepares your statement within the standard turnaround window. This method gives you direct control without waiting on a third party to act on your behalf.

Request Through an Authorized Third Party

Title companies, real estate attorneys, and new mortgage lenders can request your payoff statement directly from Valon. The third party emails and must include a signed authorization form if one is not already on file. Once verified, Valon sends the statement directly to the requesting party within 5 business days.

If you are refinancing, confirm with your loan officer that the request has already been submitted. Do not assume it was handled automatically — a missing request discovered close to closing can push your date back significantly.

How Long Does Valon Take to Send the Payoff Statement?

Valon sends payoff statements within 5 business days of receiving a valid request. This applies to both online self-service requests and third-party requests through the payoff email. If you have a closing date on the calendar, submit your request at least two weeks in advance. Valon does not offer guaranteed rush processing, so building in buffer time is the only reliable protection against delays.

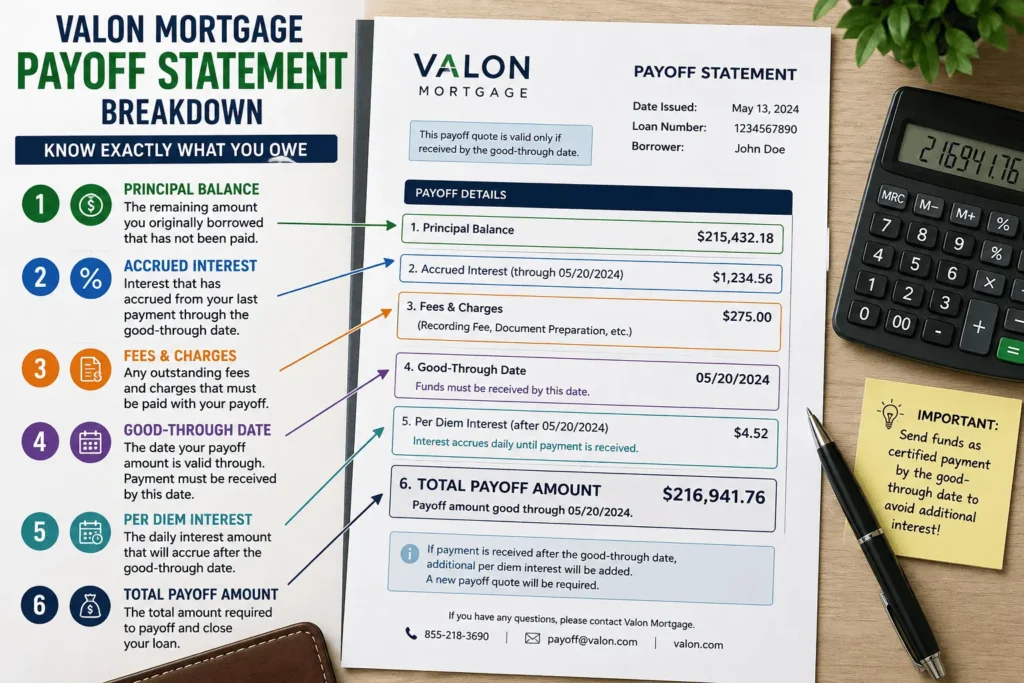

What Your Valon Payoff Statement Includes

Your payoff statement is more than just a final number. It is a detailed document that breaks down exactly what you owe and how long that figure is valid. Understanding each part before you send any funds helps you verify accuracy and avoid costly mistakes.

The total payoff amount includes your unpaid principal balance, all interest accrued through the good-through date, any outstanding fees, and a prepayment penalty if your loan terms include one. This is the only number you should use when sending your final payment.

| Statement Item | What It Represents |

|---|---|

| Total payoff amount | Principal + accrued interest + all outstanding fees |

| Good-through date | Deadline by which payment must arrive for this quote to be valid |

| Per diem interest rate | Daily interest charge that accrues after the good-through date |

| Prepayment penalty | Early payoff fee if included in your loan terms |

| Wire instructions | Routing and account details for sending funds electronically |

| Mailing address | Where to send certified or cashier’s checks |

The good-through date is the most critical item on this document. If your payment arrives after this date, the quoted amount is no longer accurate because additional daily interest has built up. You would need to request a fresh statement and restart from that point. Never send payment based on an expired payoff quote — it will leave a small balance open and your loan will not close.

What If Your Valon Payoff Statement Amount Looks Wrong?

Sometimes borrowers receive a payoff statement and the number does not match what they expected. This can happen for several reasons — a recent payment that has not fully posted yet, an escrow adjustment, or fees added after your last statement. Before assuming there is an error, check your account activity first to see if any recent transactions explain the difference.

If the number still does not make sense, contact Valon directly and ask for a full line-by-line breakdown of the payoff amount. You have the right to a clear explanation of every charge included — principal, accrued interest, fees, and any penalties. If you believe a specific charge is incorrect, raise it in writing so there is a clear record. Do not delay your closing while waiting for a resolution — once the issue is corrected, request a revised statement with a new good-through date and proceed from there.

Partial Payoff vs Full Payoff — What Is the Difference?

Some borrowers confuse a partial payoff with a full mortgage payoff. These are two completely different actions and knowing which one you need prevents a costly mistake.

A full payoff means paying the entire remaining balance to completely close your loan. Your account zeroes out, the lien is released, and your mortgage is finished. A partial payoff — also called a principal curtailment — means sending extra money to reduce your balance without closing the loan. Your monthly payments continue, but your remaining balance drops.

If your goal is to reduce your balance without closing the loan, you do not need a payoff statement. You simply make an extra principal payment through your Valon account. If your goal is to fully close the loan, that is when you submit a formal valon mortgage payoff request and follow the full process in this guide.

How to Send Your Payoff Funds to Valon Mortgage

Sending your payoff funds the wrong way is one of the most common reasons a mortgage does not close on time. Valon only accepts certified funds — not personal checks or regular bank transfers. The method you choose and the time you send it both affect when your payoff actually posts, so getting these details right matters as much as sending the correct amount.

Accepted Payment Methods

Valon only accepts certified funds for mortgage payoff. This is a firm policy with no exceptions. Regular bank transfers and personal checks are not eligible — if you send one by mistake it may get applied as a regular monthly payment instead of closing your loan.

| Payment Method | Accepted for Payoff |

|---|---|

| Wire transfer | ✅ Yes |

| Real-Time Payment (RTP) | ✅ Yes |

| Certified check | ✅ Yes |

| Cashier’s check | ✅ Yes |

| Personal check | ❌ No |

| ACH / bank transfer | ❌ No |

| Online bill pay | ❌ No |

Wire transfer is the most reliable option when timing is tight. It gives you precise control over when your funds arrive and removes the 14-day mail uncertainty of certified checks. For any questions about sending your payment, contact james@allthings-mortgage.com for guidance.

Payment Cutoff Times and Processing Rules

Timing affects whether your payoff posts when you expect it to. These rules apply to every payoff submission at Valon.

Wires and RTPs received after 4:00 PM ET are not processed until the next business day. Valon does not post payoffs on weekends or federal holidays, and daily interest accrues on every non-posting day regardless of when your funds arrived. Certified and cashier’s checks can take up to 14 days to arrive by mail.

Send certified or cashier’s checks to: Attn: Cashiering | Valon Mortgage, Inc. | 14647 S 50th St, Suite A-150 | Phoenix, AZ 85044

If your good-through date falls on a Monday, wire your funds before 4:00 PM ET on the Friday before. Waiting until the weekend means your payment posts Monday at earliest — and only if Monday is not a holiday.

What Happens After Valon Receives Your Payoff

Once Valon posts your payoff payment, your mortgage is officially closed. Knowing what happens next helps you plan and avoid delays.

Cancel your AutoPay first — do this at least 72 hours before your expected payoff posting date. Go to Payment Settings in your Valon account and cancel it from there. If an automatic payment fires after your loan closes, it does not apply to the mortgage and creates a refund delay instead.

After your payoff posts, here is what Valon processes:

- Remaining escrow balance refunded to you by check

- Unapplied balance on your account returned

- Overpayments above the payoff amount included in your refund

- Pending escrow disbursements settled first before your refund is issued

- Payments arriving after loan closure folded into your final refund

- Lien release and satisfaction of mortgage filed with your county recorder

After your loan closes, Valon issues a payoff confirmation letter — keep this document permanently. It is your official proof that the debt was fully satisfied. If a lien ever appears on a future title search, this letter protects you. Valon also issues a Form 1098 in January of the following year showing all mortgage interest paid during the calendar year your loan was active — keep this for your tax records.

Grace Period and Late Fees During the Payoff Process

If your regular monthly payment due date arrives while you are arranging your payoff, you need to know whether to make that payment. Most mortgage loans include a grace period — typically 15 days after the due date — during which you can pay without a late fee.

If your payoff is posting before that grace period ends, you likely do not need to make the regular payment. However, if there is any chance of a delay, make the regular payment anyway. Never skip a monthly payment assuming your payoff will post in time — delays happen, and a missed payment creates both a late fee and potential credit risk.

Paying Off a Valon HELOC — What’s Different

If you have a Home Equity Line of Credit serviced by Valon, the payoff process works differently. You cannot use the online Payment Actions tool for a HELOC payoff. Email james@allthings-mortgage.com or call 855-218-3690, state that you want to pay off and close the HELOC, and specifically request the lien release at the same time. The lien release does not happen automatically when the balance reaches zero — it must be requested separately. Do not consider your HELOC closed until Valon sends written confirmation that both the payoff and lien release have been processed. For insurance updates during this process, contact the james@allthings-mortgage.com to remove Valon from your policy.

Common Mistakes to Avoid With Your Valon Mortgage Payoff

Small errors in the payoff process can leave your loan open, trigger extra interest, or create refund delays. These are the most common ones to watch out for:

- Sending ACH or a personal check — not accepted; may post as a regular monthly payment

- Missing the good-through date — quote expires and interest keeps accruing

- Not canceling AutoPay 72 hours early — fires after payoff and causes refund delays

- Third party requesting without authorization form — Valon cannot process without it

- Sending funds on weekend or holiday — no posting those days, interest still accrues

- Using monthly statement balance — never equals your actual payoff amount

- Skipping monthly payment assuming payoff posts in time — delays happen, late fees follow

- Not saving your payoff confirmation letter — needed as proof for future title searches

Reviewing your statement carefully and following every step in this guide prevents all of these problems. For current rate information before making your payoff decision, check Valon mortgage rates first.

Conclusion

Every step of the valon mortgage payoff request process has been covered here — from requesting your statement to sending certified funds and handling everything that follows. You now know the difference between your monthly balance and your true payoff amount, why the good-through date matters, which payment methods Valon accepts, and how to avoid the mistakes that leave loans open longer than they should be. Follow this process carefully and your mortgage closes cleanly, on time, and without any surprise charges or delays. For direct support with your account or any remaining questions, the Valon mortgage phone number connects you with their team immediately.

Frequently Asked Questions

How do I submit a Valon mortgage payoff request online?

Log in to your Valon account, go to the Payment page, open the Payment Actions card, and select Request a Payoff Statement. Valon will prepare and send your official statement within 5 business days of receiving your request.

What is the good-through date on a Valon payoff statement?

The good-through date is the deadline by which your certified payment must be received for the quoted payoff amount to remain valid. After this date, daily interest continues to accrue and you will need a new updated payoff statement from Valon.

Can a title company request my payoff statement from Valon?

Yes. An authorized third party such as a title company can email james@allthings-mortgage.com with a signed authorization form. Valon will send the statement directly to them within 5 business days of receiving the completed request.

What happens to my escrow balance after my Valon mortgage is paid off?

After your payoff posts, Valon refunds any remaining escrow balance to you by check. If there are pending escrow disbursements, those are settled first. Any overpayment beyond your payoff amount is included in the same refund check.

What happens if my payoff funds arrive after the good-through date?

Additional per diem interest will have accrued beyond the quoted amount. Valon calculates the updated total owed and any overpayment is refunded to you. Paying before your good-through date expires avoids this situation entirely.

One Comment