Have you spent an evening scrolling through a lender’s website, hunting for a number that just never shows up? You type in your loan amount, click through a few pages, and still walk away with no clear figure. That happened to me too the first time I looked into a Guild loan. I kept waiting for a rate chart to load, and it simply never did.

This guide clears up that confusion. You will learn how Guild Mortgage interest rates actually work, why the company keeps them off its website, and what really shapes the number a loan officer quotes you. By the end, you will know exactly what to ask for and how to compare your offer against the rest of the market.

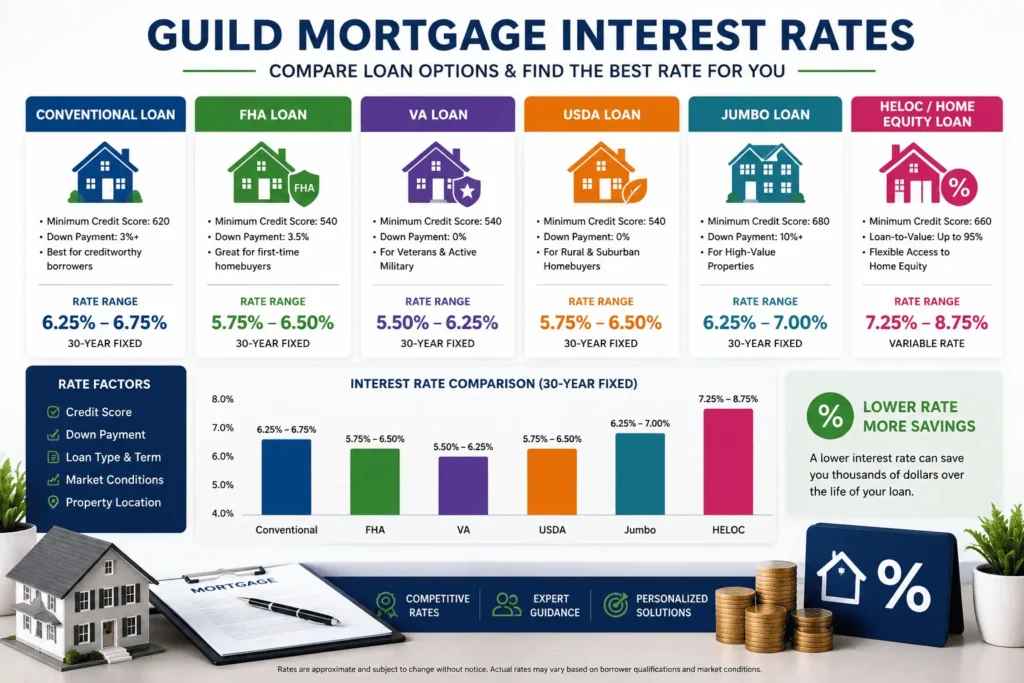

What Are Guild Mortgage’s Current Interest Rates?

Guild Mortgage does not post a public rate sheet. That is different from most large banks, and it catches a lot of shoppers off guard. Your rate depends on your credit score, your loan type, your down payment, and even your state.

As of late June 2026, national averages give a useful starting point. The average 30-year fixed mortgage sits near 6.5%, while 15-year loans average closer to 5.9%. Guild’s own pricing tends to land close to these averages, though it can run a touch higher for borrowers with thinner credit files. The only way to get your real number is to speak with a loan officer or start an application.

Today’s housing market moves fast, and a quoted number can change within hours. That is part of why Guild Mortgage interest rates are never frozen on a webpage somewhere. Treat any average you read online as a rough guide, not a guarantee, and confirm your actual offer before comparing lenders.

Why Doesn’t Guild Mortgage Show Rates Online?

This question comes up constantly, and the answer is simple. Mortgage pricing changes by the hour based on bond markets, and a posted number rarely matches what a real borrower qualifies for. Many lenders skip public rate charts for this exact reason.

Guild also prices loans individually using your full financial picture. A generic rate chart based on perfect credit would not reflect what most buyers actually pay. Instead, Guild asks you to start a short application or call a branch, which lets a loan officer pull your real numbers and quote something accurate. It takes a few extra minutes, but the quote you get back is built for your situation, not a stranger’s.

Guild Mortgage Interest Rates by Loan Type

Pricing also shifts depending on which loan program you choose. Government-backed loans, jumbo loans, and home equity products all carry their own rate ranges. Here is a quick breakdown of what shapes pricing across Guild’s main loan categories.

| Loan Type | Typical Minimum Credit Score | Rate Tendency |

|---|---|---|

| Conventional | 620 | Tracks national average closely |

| FHA | 540 | Often slightly lower than conventional |

| VA | 540 | Usually the lowest of all programs |

| USDA | 640 | Close to FHA pricing |

| Jumbo | 680 | Can run higher or lower depending on lender appetite |

| Home Equity/HELOC | 660 | Tied to prime rate, often variable |

Conventional loan rates

Conventional loans make up the bulk of Guild’s business. Pricing here usually mirrors the broader market, since these loans get sold to Fannie Mae or Freddie Mac. A higher credit score and a bigger down payment will pull your number down noticeably.

Borrowers with scores above 740 tend to see the best conventional pricing. Below 660, expect a meaningful rate bump. Discount points can also buy your rate down if you have extra cash at closing.

FHA loan rates

FHA loans through Guild often come in slightly below conventional pricing. This makes sense, since the FHA insures part of the loan and reduces the lender’s risk. The tradeoff is mortgage insurance, which adds to your monthly cost even with a lower rate.

Guild allows credit scores as low as 540 for FHA loans with a 10% down payment, and 580 with just 3.5% down. That flexibility makes FHA loans popular with first-time buyers who are still building credit.

VA loan rates

VA loans usually carry the lowest rates Guild offers. There is no down payment requirement and no private mortgage insurance, which keeps the overall cost low for eligible veterans and service members. Guild also accepts scores as low as 540 for this program.

Because VA loans are government-backed, lenders take on less risk and can price them aggressively. If you qualify through military service, this is almost always worth exploring before any other loan type.

USDA loan rates

USDA loans target buyers in eligible rural and suburban areas with low to moderate income. Pricing tracks closely with FHA loans, and the program allows 100% financing with no down payment. Guild typically asks for a 640 credit score here.

This program works well for buyers who found a home outside a major city and meet the income limits. The savings on the down payment alone can offset a slightly higher rate compared to VA loans.

Jumbo loan rates

Jumbo loans cover amounts above the conforming loan limit, which sits above $800,000 in most counties for 2026. Guild requires a 680 credit score for these loans, and pricing can swing more than conventional loans because fewer investors buy jumbo debt.

Some borrowers actually see jumbo rates close to or below conventional rates, depending on Guild’s current investor demand. It pays to ask your loan officer directly how jumbo pricing compares the week you apply.

Home equity loan and HELOC rates

Guild also offers home equity loans and a HELOC for homeowners who want to tap built-up equity. Both products require a 660 minimum credit score. The home equity loan lets you borrow a lump sum up to 90% of your equity, while the HELOC offers a revolving line up to 95%.

HELOC rates are usually variable and tied to the prime rate, so your payment can shift over time. Guild does offer a fixed-rate HELOC option for borrowers who want predictable payments instead.

Are Guild Mortgage’s Interest Rates Competitive?

Guild’s average rate in recent federal data has landed slightly above the national median, but the gap is usually small. What sets Guild apart is not the headline rate. It is the stack of programs that lower your upfront cost, like reduced down payment options and closing cost credits.

A borrower focused only on the rate might miss real savings elsewhere. Closing cost assistance, gift cards toward a down payment, and temporary rate buydowns can shrink your total cost even when the listed rate looks average. For a full breakdown of fees and overall value, this Guild Mortgage review digs into pricing alongside customer feedback.

The honest answer is that competitiveness depends on your profile. A borrower with strong credit and a steady income might find better pricing through a big bank. A first-time buyer using Guild’s assistance programs could come out ahead even with a slightly higher base rate.

When you weigh Guild Mortgage interest rates against other lenders, look past the headline number. Add up the closing costs, lender fees, and any cash assistance on both sides before deciding which offer actually saves you more over the life of the loan.

What Determines Your Guild Mortgage Interest Rate?

Several factors combine to set your final number, and none of them work alone. Your credit score carries the most weight, since it signals how reliably you have repaid debt in the past. A 740 score versus a 620 score can mean a difference of half a point or more.

Your down payment matters almost as much. Putting down 20% or more usually unlocks better pricing and skips mortgage insurance entirely. Loan term also plays a role, since shorter terms like 15 years carry lower rates than 30-year loans.

Loan type and location round out the list. Government-backed loans price differently than conventional ones, and some states carry slightly different average costs due to local market conditions. Debt-to-income ratio matters too, since lenders want proof you can comfortably handle the new payment.

In short, Guild Mortgage interest rates are never set by one single factor. Lenders blend your credit, your down payment, your loan type, and your overall debt picture into one final number, which is why two neighbors buying similar homes can end up with very different rates.

How to Get a Lower Interest Rate from Guild Mortgage

Guild offers several built-in programs designed to reduce your costs without forcing you to wait years for the market to shift. These tools work alongside your base rate rather than replacing it. Below are the three most useful options worth asking your loan officer about, each one capable of softening Guild Mortgage interest rates in a different way.

Temporary buydowns (Payment Advantage and Payment Advantage Plus)

These programs lower your payment for the first year or two of the loan, then return to the standard rate. Payment Advantage typically reduces your rate by 1% in year one, while Payment Advantage Plus can stretch that relief across two years. This gives new homeowners breathing room while they settle into a new payment.

It works well for buyers expecting their income to rise soon, or those who plan to refinance once rates drop. The seller or builder often covers the cost of the buydown, so it does not always come out of your pocket.

Complete Rate for borrowers with thin credit

Guild’s Complete Rate program looks at alternative credit data like rent payments, utility bills, and even car insurance history. This helps borrowers with limited traditional credit history still qualify for solid pricing on FHA, VA, and USDA loans. It is a smart option if you pay your bills on time but have not built a long credit file yet.

3-2-1 Home Plus and closing cost assistance

This program pairs a 3% down payment with up to $2,500 in closing cost help and a $2,000 gift card toward home improvements. While it does not directly change your rate, it reduces the cash you need at closing, which frees up money elsewhere. Combined with a temporary buydown, this stacking approach can make a real dent in your first-year costs.

How Guild’s Lock and Shop Rate Lock Works

One of Guild’s standout features is the Lock and Shop program. It lets you lock in your rate for up to 120 days while you are still house hunting, which protects you if rates climb during your search. If rates happen to drop instead, Guild includes a one-time float-down option so you are not stuck paying more than necessary.

This matters in a market where rates can shift several times in a single week. Locking early removes one major variable from your home search, letting you focus on finding the right property instead of watching the bond market.

How to Get a Personalized Guild Mortgage Rate Quote

Since Guild does not publish rates, getting a real number means starting a conversation. You can begin an application online through Guild’s website, or call a local branch directly. Either path connects you with a loan officer who will ask about your income, credit, and target loan amount.

Come prepared with recent pay stubs, your last two years of tax returns, and an idea of your target home price. This speeds up the process and gets you a more accurate number on the first call. If you already have a Guild loan and want to check your account details before refinancing, this guide to managing your Guild account online walks through the login steps. For general support questions along the way, Guild’s customer service contact options cover every available channel. You can also send general questions about this guide to james@allthings-mortgage.com.

Guild Mortgage Refinance Rates

Guild offers both rate-and-term refinancing and cash-out refinancing for current homeowners. Rate-and-term refinancing swaps your existing loan for a new one with better terms, while cash-out refinancing lets you pull equity out as cash. National refinance rates today run slightly above purchase rates, often by two to three tenths of a percentage point.

If you closed your original loan when rates were higher, current Guild Mortgage interest rates on a refinance might still beat what you are paying now. It is worth checking even if you assume the timing is wrong, since pricing shifts week to week.

A useful first step before refinancing is running the numbers through a refinance calculator to see whether the new payment actually saves you money. Guild’s Payment Protection Program allows a refinance with no lender fees if rates drop significantly after your original closing, which is worth asking about if you closed your loan in the past year or two. To see how a new rate would change your monthly cost, pairing a payment calculator with your specific loan numbers gives you the clearest picture before you commit. This breakdown of Guild’s monthly payment options is also worth reading if you want to understand how a refinance might shift your due date or payment method.

Conclusion

As promised at the start, you now have a full picture of how Guild Mortgage interest rates actually work behind the scenes. You know why the numbers stay off the website, what shapes your personal quote, and which programs can soften your upfront costs. The next smart move is reaching out to a loan officer with your real numbers in hand. Comparing that quote against two or three other lenders will tell you whether Guild’s offer truly fits your budget.

Frequently Asked Questions

Does Guild Mortgage publish its interest rates online?

No, Guild does not post current rates on its site. You need to apply or speak with a loan officer to get a personalized quote based on your credit and loan details.

What credit score do I need for the best Guild Mortgage rate?

A score above 740 typically unlocks Guild’s best conventional pricing. Government-backed loans like FHA and VA allow much lower scores, though the rate may run slightly higher.

Can I lock my rate before finding a house?

Yes, Guild’s Lock and Shop program locks your rate for up to 120 days while you search. It includes a one-time float-down if rates drop during that window.

Are Guild’s refinance rates different from purchase rates?

Refinance rates often run slightly higher than purchase rates, typically by a fraction of a percent. The exact gap shifts with market conditions, so check current pricing when you apply.

Does a bigger down payment lower my Guild Mortgage rate?

Yes, putting down 20% or more usually earns better pricing and removes the need for mortgage insurance. Even a smaller increase in your down payment can shave points off your offered rate.